One of the most common points of confusion for working professionals in India is the difference between the CTC mentioned in an offer letter and the amount that actually gets credited to their bank account each month. This article breaks down the structure of CTC, explains each component clearly, and helps readers understand where their salary goes and why.

What Is CTC?

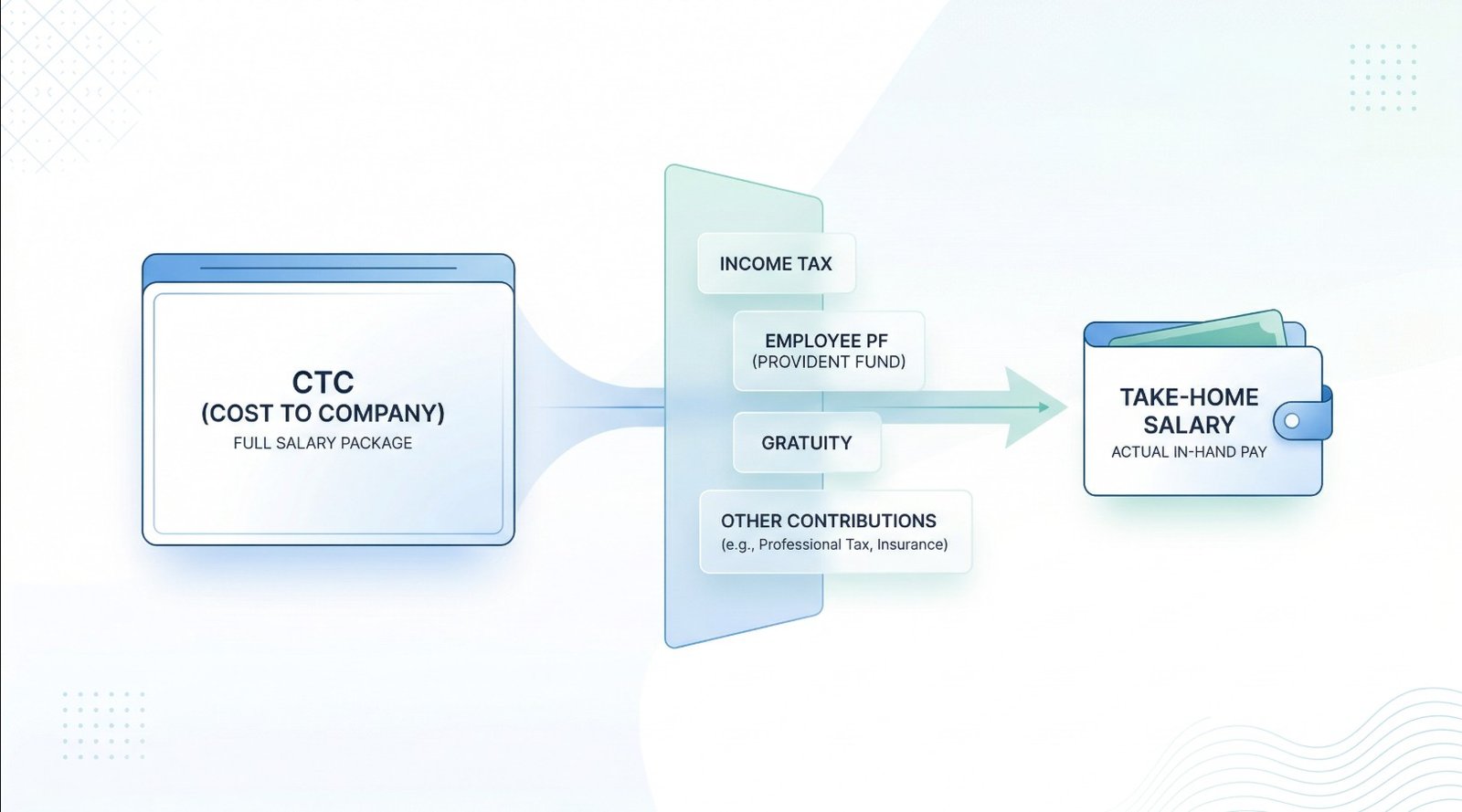

CTC is an acronym for Cost to Company. It represents the total annual expenditure an employer incurs on an employee. This includes not just the monthly salary, but also contributions toward statutory savings, benefits, and other allowances.

When a company states a CTC of ₹20 LPA (Lakhs Per Annum), it means the total cost of employing that individual across all heads, some of which are paid monthly, some held for the future, and some directed toward statutory obligations.

CTC is not the same as the amount deposited into an employee’s account each month. That figure is called take-home salary or in-hand salary, and it is always lower than CTC.

Components of CTC

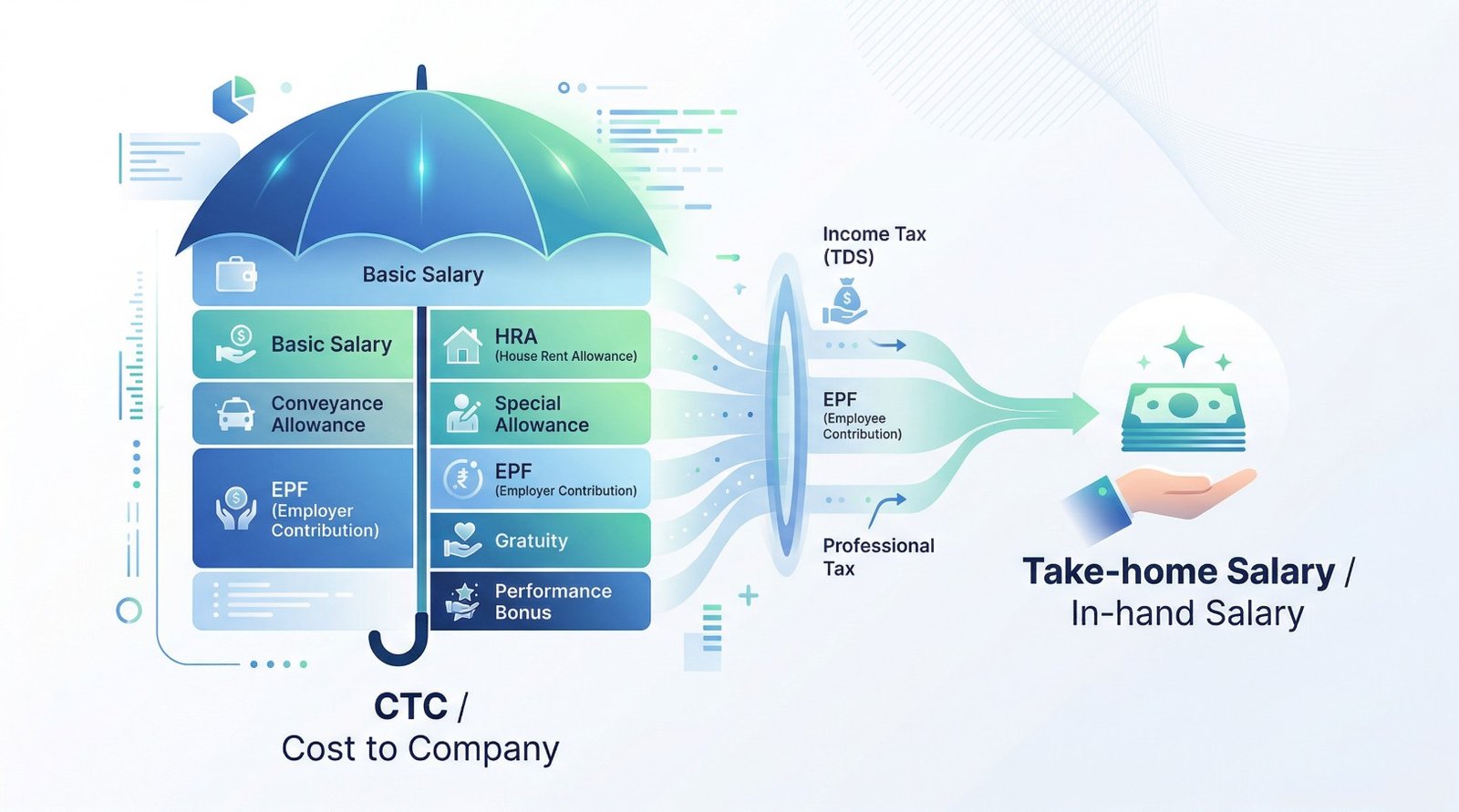

1) Basic Salary

Basic salary is the fixed core component of the compensation structure. It is usually between 40% and 50% of the total CTC and is fully taxable under Indian income tax law.

Under the Code on Wages, 2019, the government mandated that the basic salary must be at least 50% of total remuneration. This move was intended to reduce the practice of artificially suppressing Basic salary to lower statutory contributions like the Provident Fund, Gratuity, Leave encashment, Bonus, etc.

2) House Rent Allowance (HRA)

HRA is a component provided to help employees meet rental expenses. It is typically calculated as a percentage of Basic salary:

• 50% of the basic salary for employees in metro cities (Mumbai, Delhi, Kolkata, Chennai)

• 40% of the basic salary for employees in non-metro locations

HRA is partially exempt from income tax for employees who pay rent, subject to conditions specified under Section 10(13A) of the Income Tax Act. Employees living in their own homes or with family without paying rent do not qualify for this exemption, and the full HRA becomes taxable in their case.

3) Special Allowance

Special allowance is the residual amount that fills the gap between the defined components and the total CTC. It is fully taxable and does not carry any specific statutory benefit or exemption. Its presence in the salary structure primarily serves to complete the CTC computation.

4) Provident Fund (PF)

Employees’ Provident Fund (EPF) is a statutory savings mechanism governed by the Employees’ Provident Fund and Miscellaneous Provisions Act, 1952. Both the employer and the employee contribute 12% of the employee’s Basic salary to the EPF account each month.

The employer’s contribution of 12% is included within the CTC figure. This is a significant reason why the CTC appears higher than the actual take-home amount. These funds are accessible to the employee upon retirement, resignation after a qualifying period, or under specific permitted withdrawal conditions.

With higher Basic salaries under the new Labour Codes, EPF contributions increase proportionally, strengthening long term financial security even if short-term take-home is marginally lower.

5) Gratuity

Gratuity is a statutory benefit payable under the Payment of Gratuity Act, 1972. It is a lump sum amount paid by the employer when an employee leaves the organization after completing at least five continuous years of service. It is calculated as 15 days’ Basic salary for every year of completed service. Although gratuity accrues over the tenure of employment, it forms part of the CTC structure from day one.

6) Other Allowances and Benefits

CTC may also include the following components, depending on the employer’s salary policy:

• Medical Allowance – provided for healthcare-related expenses

• Conveyance Allowance – for commuting costs

• Leave Travel Allowance (LTA) – partially exempt from tax for eligible travel within India

• Performance Bonus – variable pay linked to individual or company performance

The inclusion and value of these components vary by organization, role, and industry sector.

Deductions That Reduce Take-Home Salary

1) Tax Deducted at Source (TDS)

Employers are required to deduct income tax at source before crediting the monthly salary. The amount deducted depends on the employee’s total taxable income for the year and the tax regime they have opted for. (Ref: Section 192, Income Tax Act)

As of Budget 2023, the New Tax Regime is the default option. Employees may, however, opt for the Old Tax Regime if it is more beneficial, given deductions available under sections such as 80C, 80D, and exemptions like HRA.

2) Professional Tax

Professional tax is a state-level levy applicable in several Indian states. The amount typically ranges between ₹150 and ₹200 per month, depending on the state and income bracket. It is a relatively minor deduction but is reflected on every payslip.

3) Employee’s PF Contribution

As noted above, 12% of the basic salary is deducted from the employee’s gross pay each month and deposited into their EPF account. While this amount belongs to the employee, it is not immediately accessible and forms part of their long term savings.

How Take-Home Salary Is Calculated

The following formulas provide a standard framework for understanding the relationship between CTC and take home salary:

Gross Salary = CTC − Employer’s PF Contribution − Gratuity − Other Non-Cash Benefits

Take-Home Salary = Gross Salary − (Employee’s PF + TDS + Professional Tax)

For illustrative purposes: on a CTC of ₹10 LPA, the monthly take-home salary typically falls in the range of ₹65,000 to ₹72,000, depending on the city of residence, applicable tax regime, and specific salary structure. Actual figures will vary based on individual circumstances and employer policy.

Impact of the New Labour Codes

The Government of India has consolidated multiple labour laws into four new Labour Codes: the Code on Wages, the Industrial Relations Code, the Code on Social Security, and the Occupational Safety, Health and Working Conditions Code. Once fully implemented, these codes are expected to bring meaningful changes to how salary structures are designed:

• Higher Basic salary thresholds will lead to proportionally higher PF, Gratuity, Leave encashment and bonus contributions.

• Clearer definitions of wages will reduce ambiguity in how CTC is structured.

• Extended social security coverage for gig and platform workers.

Employees may notice a slight reduction in short-term take-home salary as Basic salary proportions increase. However, this also means stronger statutory savings and greater long-term financial security.

Key Takeaways

• CTC is the employer’s total cost of employment — it is not the same as take-home salary.

• Several components within CTC are directed toward future savings or statutory obligations.

• Deductions, including TDS, employee PF, and professional tax, reduce the gross salary to the amount actually received.

• The New Tax Regime is the default option from FY 2023-24 onwards, though employees may evaluate the Old Regime based on their eligible deductions.

• The new Labour Codes, once implemented, will further reshape salary structures across organisations.

References

[1] Code on Wages, 2019 – Ministry of Labour and Employment (Official Act): labour.gov.in – The Code on Wages, 2019

[2] Employees’ Provident Fund Organisation (EPFO) – Official Website: www.epfindia.gov.in

[3] EPFO – About EPFO and EPF Act, 1952: epfindia.gov.in/site_ en/AboutEPFO.php

[4] Income Tax Department – Section 10(13A) HRA Exemption & Section 80C: incometax.gov.in

[5] Income Tax Department – Official Portal: www.incometax.gov.in

[6] Ministry of Labour and Employment – Labour Reforms Overview (PIB): pib.gov.in – Labour Reforms: Code on Wages & Four Labour Codes

[7] Code on Wages 2019 – PRS Legislative Research Summary: prsindia.org – Code on Wages, 2019

[8] Payment of Gratuity Act – Ministry of Labour: www.labour.gov.in

Readers Note:

TalentCo HR Services LLP is an HR consulting and solutions company offering services across HR operations, compliance, liasoning, payroll management, and HR technology through its proprietary platform — ABStart.

This article is intended for general informational and educational purposes only. Labour laws, tax regulations, and compliance requirements are subject to change based on government notifications and jurisdictional updates. Readers are advised to independently verify current regulations or consult qualified professionals before making any business or financial decisions.

Our role is to simplify and present complex HR and payroll concepts in a comprehensible manner for business owners, HR professionals, and employees.