India’s four Labour Codes have been passed by Parliament. Several states have already published their draft rules, and the central government has indicated intent to operationalize the Codes, with implementation timelines dependent on state-level rule finalisation. For Indian SMEs, this is no longer just a future concern — it requires proactive preparation from businesses ahead of implementation that demands structured action.

Understanding What Has Changed

The four Labour Codes — the Code on Wages, 2019; the Industrial Relations Code, 2020; the Code on Social Security, 2020; and the Occupational Safety, Health and Working Conditions Code, 2020 — consolidate 29 existing central labour laws. The changes they introduce are not cosmetic.

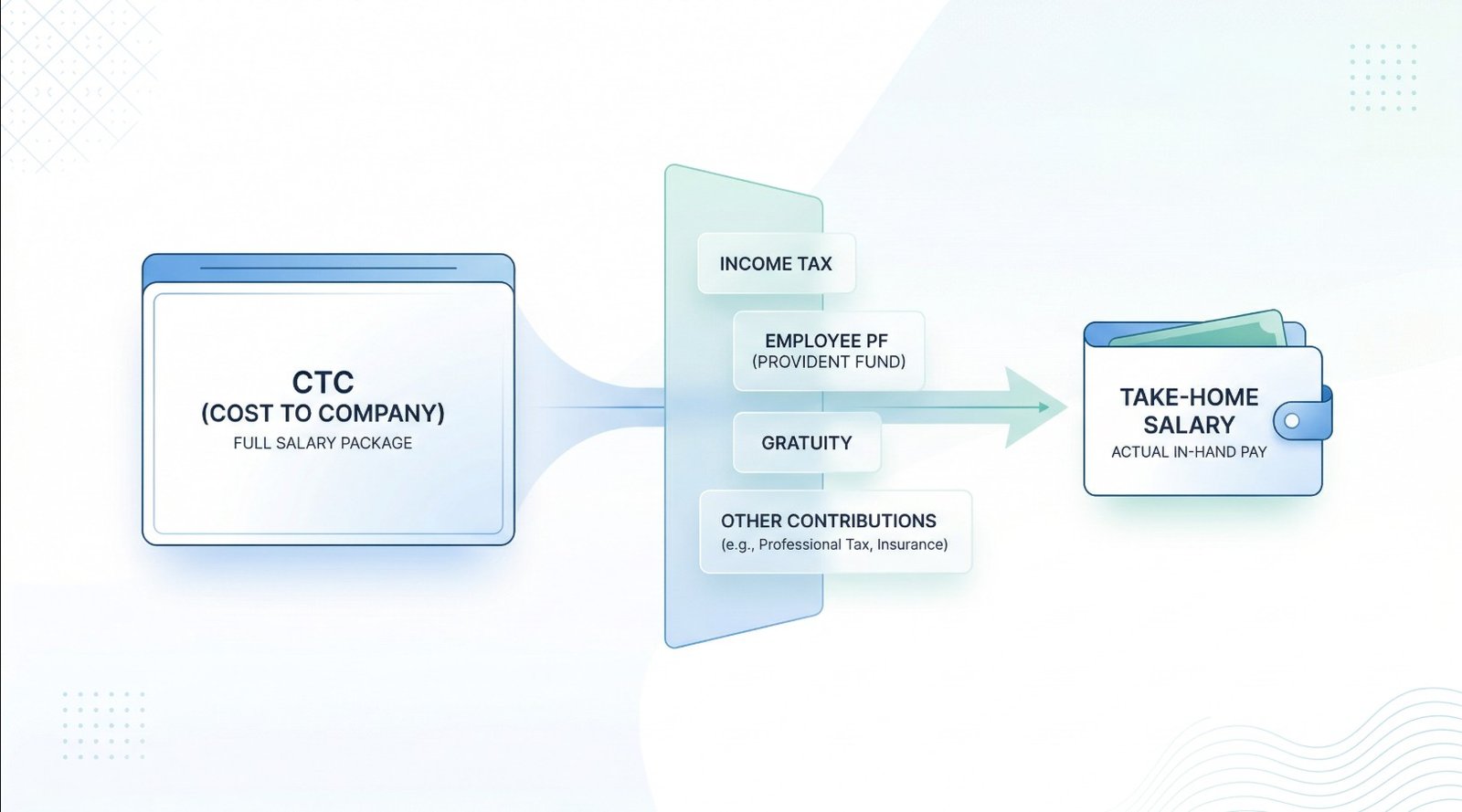

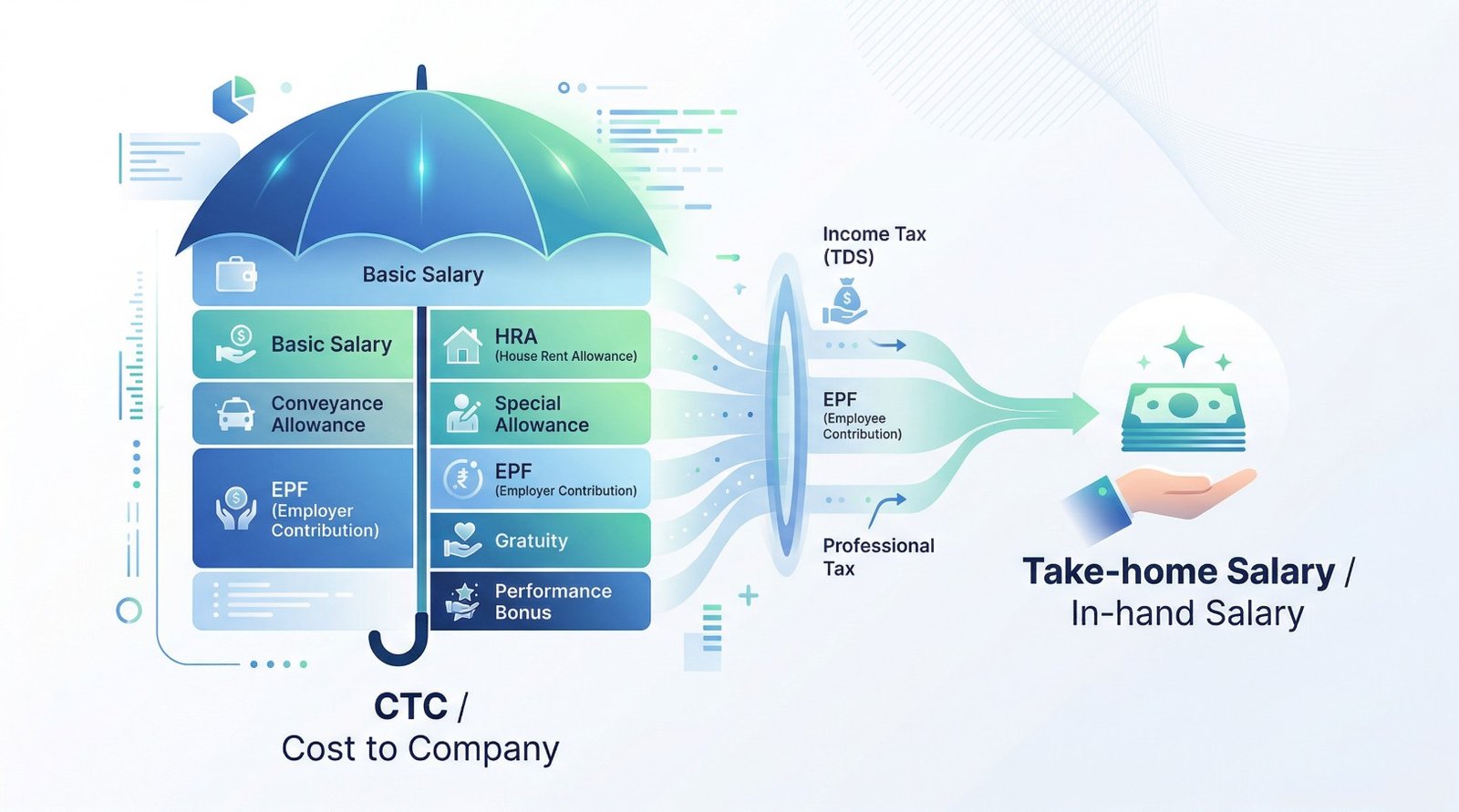

The Code on Wages, 2019, introduces a revised definition of wages with specified inclusions and exclusions, along with a 50% threshold for allowable exclusions. This may impact how PF contributions are computed, as wage structures align with the revised definition. Under the new definition, if allowances beyond the excluded categories exceed 50% of total CTC, the excess must be treated as wages, increasing the PF base. For organisations that have structured salary to keep Basic low, this will require a fundamental redesign.

The Code on Social Security, 2020, expands the ambit of EPF and ESI coverage. It also introduces new categories of workers, including gig and platform workers, into the social security framework. SMEs working with contract and gig labour must account for these obligations as rules are notified.

Where the Compliance Gap Is Largest for SMEs

Most Indian SMEs face three concentrated areas of risk under the new framework:

- Salary structure misalignment: CTC templates designed to minimise PF deductions will not hold under the new wage definition. Retrospective liability for PF arrears under Section 14B of the EPF Act, 1952, can attract damages of up to 100% of the arrears due.

- Leave and working hours: The Codes standardise definitions for working hours, overtime thresholds, and leave entitlements. SMEs operating on informal leave policies without documented records will find it difficult to demonstrate compliance during audits.

- DPDP Act obligations on employee data: The Digital Personal Data Protection Act, 2023, requires that employee data — including Aadhaar, bank details, and health records — is stored securely, processed lawfully, and deleted when no longer required. Unsecured or poorly managed data storage practices may not meet these standards.

A Practical Compliance Roadmap

The transition to Labour Code compliance does not need to be disruptive. It does, however, need to be structured. The following sequence is a practical starting point for SMEs:

- Audit your current salary architecture: Map each CTC component against the new wage definition under the Code on Wages. Identify whether Basic salary, as currently structured, meets the 50% threshold requirement.

- Recalculate PF and ESI liability: Once wage definitions are corrected, rerun PF and ESI calculations. Determine whether contribution amounts will change and plan for the revised employer cost.

- Document all leave and attendance policies: Convert informal leave practices into written, time-stamped policies. Ensure attendance and leave records are maintained digitally and are audit-ready.

- Secure employee personal data: Move employee data from unencrypted shared files or email threads to a system that provides access controls, audit logs, and defined data retention policies.

- Update employment contracts and standing orders: The Industrial Relations Code alters provisions around notice periods, layoffs, and standing orders. Contracts should be reviewed by a qualified HR or legal professional and updated accordingly.

The Role of Structured HR Systems

Structured HRMS platforms built for Indian compliance — such as ABStart, are designed around these regulatory requirements. Its payroll engine automates PF, ESI, and TDS calculations, and its record-keeping module maintains audit-ready documentation. For SMEs looking to move from manual spreadsheets to a compliant operation, this kind of purpose-built infrastructure reduces both the transition effort and the ongoing compliance risk.

Key Takeaways

- The four Labour Codes are passed legislation; full enforcement is expected to deepen through 2026 as states finalise rules.

- Salary structures that suppress Basic wages to reduce PF liability will be directly non-compliant with the Code on Wages, 2019.

- Regulatory scrutiny may increase as compliance frameworks evolve; inaccurate contribution records carry significant retrospective penalties.

- The DPDP Act, 2023, makes informal employee data storage in spreadsheets a compliance liability — penalties for non-compliance can be significant, depending on the severity of the violation.

- Structured HRMS platforms purpose-built for Indian regulatory requirements, like ABStart, convert compliance risk into controlled, audit-ready processes.

References

- Code on Wages, 2019 — Ministry of Labour and Employment

- Industrial Relations Code, 2020 — Ministry of Labour and Employment

- Code on Social Security, 2020 — Ministry of Labour and Employment

- Occupational Safety, Health and Working Conditions Code, 2020 — Ministry of Labour and Employment

- Employees’ Provident Fund Organisation — Section 14B, EPF Act, 1952

- Digital Personal Data Protection Act, 2023 — Ministry of Electronics and Information Technology

- PRS Legislative Research — Labour Codes Summary

- ESIC — Employees’ State Insurance Corporation Official Portal

Reader’s Note: TalentCo HR Services LLP is an HR consulting and solutions company offering services across HR operations, compliance, payroll management, and HR technology through its proprietary platform — ABStart. This article is intended for general informational and educational purposes only. Labour laws, tax regulations, and compliance requirements are subject to change based on government notifications and jurisdictional updates. Readers are advised to independently verify current regulations or consult qualified professionals before making any business or financial decisions.

- What Is the Standard 30-60-90-Day Onboarding Checklist for SMEs?

- Can You File Your ITR Without Form 16? Deadlines, Costs and the Regime Question for AY 2026-27

- How to choose an HRMS for your Indian SME – The questions your vendor won’t answer

- Payroll Compliance in India for SMEs – What it actually looks like on the ground

- How to Digitalise HR in your Indian SME : A Step-by-Step guide