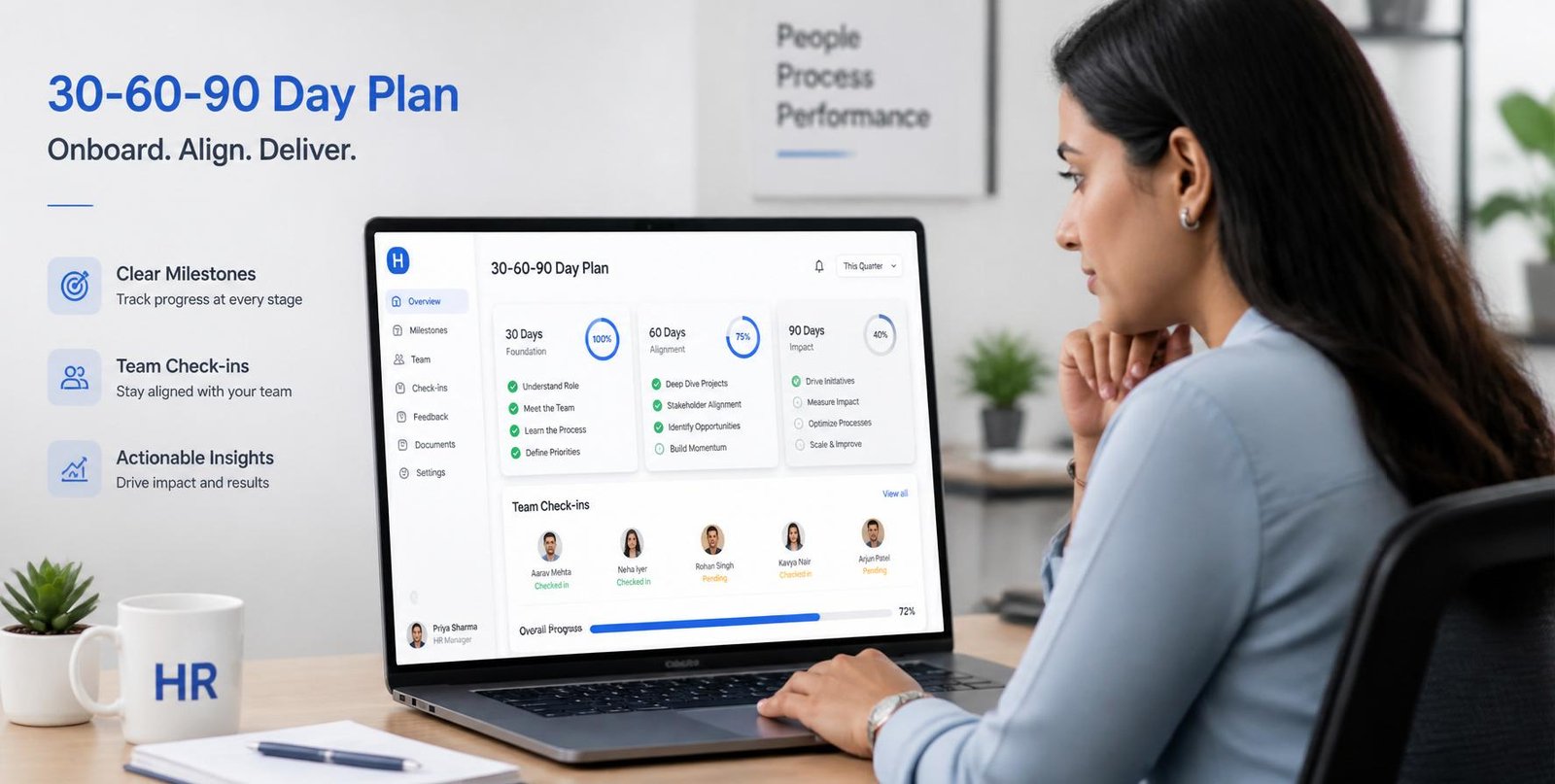

A 30-60-90-day checklist breaks onboarding into three distinct stages: orientation, application, and review. It provides new hires with clear expectations at each milestone while giving managers fixed checkpoints instead of guessing who is on track. This structured approach works exceptionally well for small and mid-sized enterprises (SMEs) in India because it requires no dedicated onboarding team—just one consistent, repeatable framework followed for every hire.

Onboarding at growing businesses often falls to whichever team member has available bandwidth that week. This leads to inconsistent instructions, missed compliance steps, and unclear performance expectations. Implementing a structured 30-60-90-day onboarding plan resolves these operational gaps without adding administrative overhead, giving both full-time employees and contract workers the clarity needed to succeed.

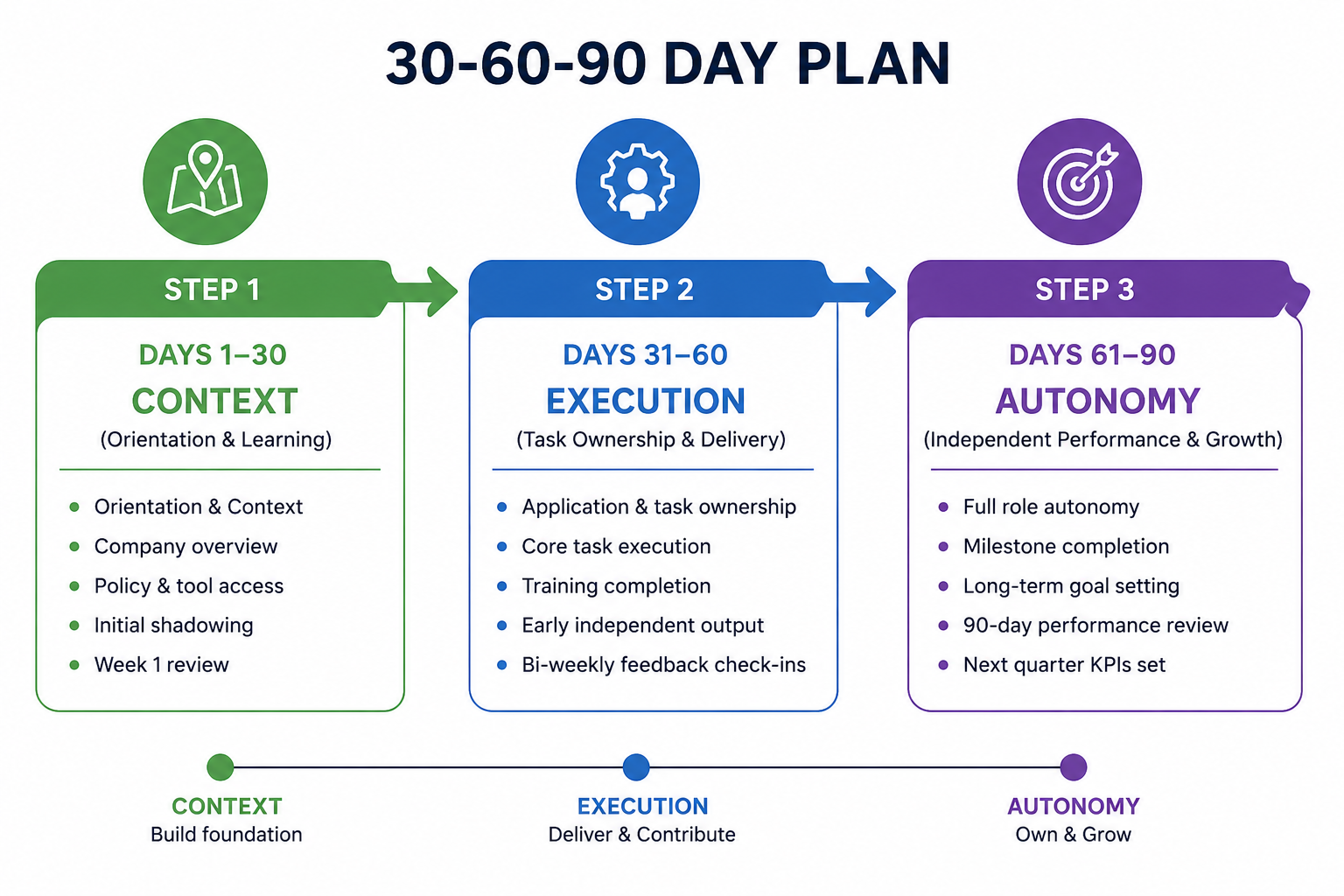

Why Does a 30-60-90-Day Onboarding Plan Matter?

Dividing the first 90 days into three structured phases provides new team members with predictable milestones rather than open-ended goals. Employees clearly understand what ‘settled in’ and ‘fully independent’ actually mean in practice. Managers gain natural checkpoints to evaluate progress instead of waiting until performance issues arise. For SMEs without a dedicated HR department, leverage simple onboarding software combined with this template to replace guesswork with a repeatable process.

1. Removes ambiguity regarding what strong progress looks like at each stage.

2. Establishes fixed manager check-ins rather than relying on memory or informal follow-ups.

3. Delivers a consistent experience across every new hire, regardless of department or manager.

4. Reduces early turnover caused by unclear expectations in the first few weeks.

“The biggest hidden tax in a growing SME isn’t overhead—it’s early turnover. When a new hire leaves in their first 90 days, you haven’t just lost salary in rupees; you’ve burned leadership energy and team momentum. A clear 30-60-90 day structure turns early uncertainty into long-term retention.”

— Rahul Dhamdere, Co-Founder, ABStart HRMS

What Should the First 30 Days of Onboarding Include?

The first 30 days must focus on orientation and context rather than immediate output. New hires need to understand company culture, role structure, and essential software tools. Expecting full productivity during this initial window often backfires, as it skips the operational foundation an employee requires to perform effectively later.

1. Company overview: Mission, organizational structure, and how their role directly contributes to business objectives.

2. Policies and processes: Leave policies, code of conduct, reporting hierarchies, and statutory compliance details.

3. Tool and software access: Email IDs, communication platforms, and role-specific software logins.

4. Role expectations: A clear breakdown of primary responsibilities and key performance metrics.

5. First assignment or shadowing: A low-stakes initial project or shadowing period to build operational familiarity before taking full ownership.

What Should Days 31–60 of Onboarding Focus On?

Days 31 to 60 mark the transition from learning to execution. Employees begin taking ownership of core tasks with regular managerial feedback to correct course early. This phase naturally highlights skill gaps, allowing managers to address training needs before they develop into larger performance obstacles.

1. Core task ownership: Assigning direct responsibility for core duties rather than observational tasks.

2. Training completion: Finalizing role-specific or compliance training initiated during month one.

3. Feedback check-ins: Conducting brief, scheduled check-ins to resolve operational roadblocks promptly.

4. Gradual independence: Reducing daily supervision as employee confidence and technical competence grow.

What Should Days 61–90 of Onboarding Include?

By days 61 to 90, the employee should operate with full autonomy. This final stage centers on formal performance evaluation—comparing actual contributions against initial benchmarks established during the first 30 days and agreeing on future development goals.

1. Autonomous execution: Full accountability for core responsibilities with minimal daily supervision.

2. Performance review discussions: Structured conversations evaluating delivered outcomes against initial expectations.

3. Quarterly progress checks: Reviewing overall growth across the entire 90-day window rather than recent weeks alone.

4. Next-stage planning: Establishing clear targets for the upcoming quarter so onboarding transitions smoothly into regular performance management.

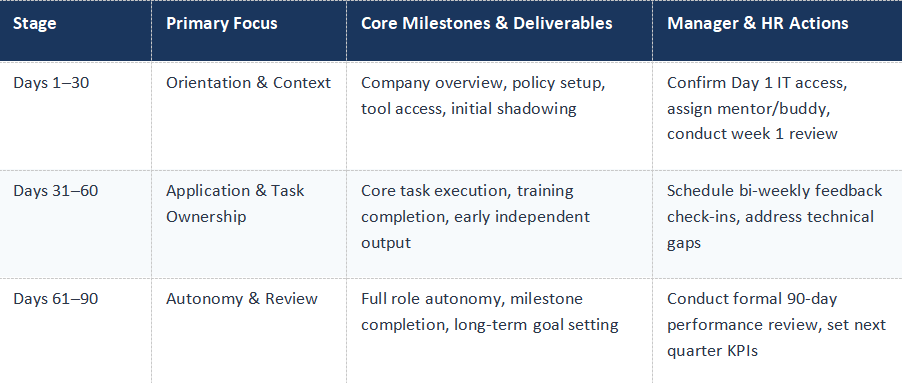

Table 1: The Master 30-60-90 Day Full-Time Employee Onboarding Framework

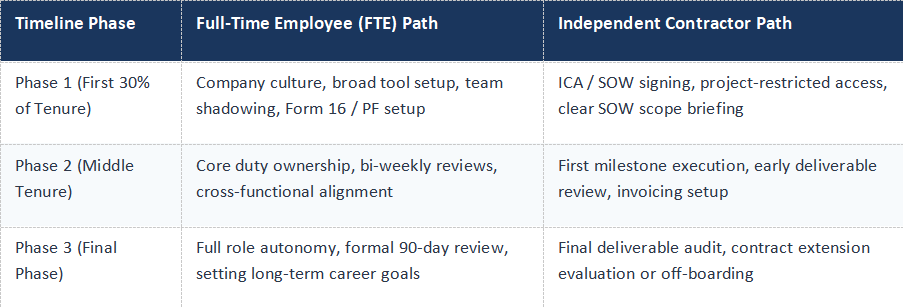

What Does a 30-60-90-Day Onboarding Checklist Look Like for Contract Workers?

Contract workers follow a similar three-phase progression, but compressed and refocused. Long-term cultural immersion matters less, whereas explicit scope clarity, fast system provisioning, and early milestone delivery matter significantly more.

Table 2: 30-60-90 Day Adaptation (Full-Time Employees vs. Independent Contractors)

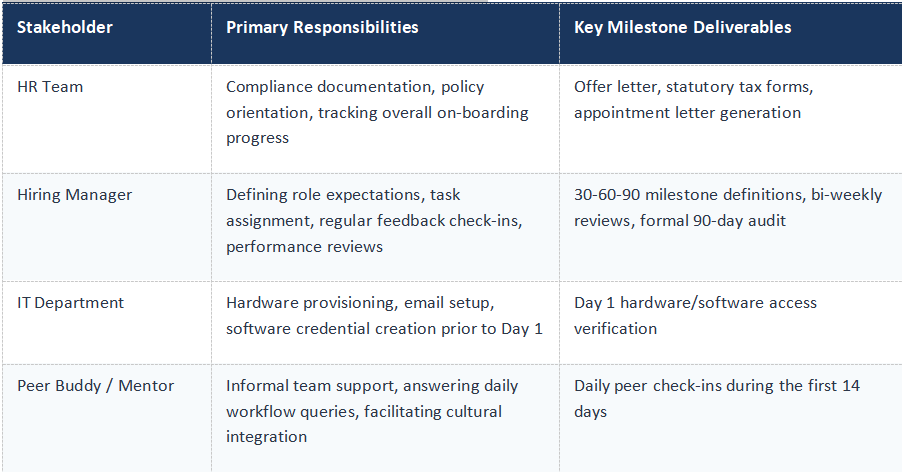

Who Owns What in Onboarding: HR, Manager, IT, and Peer Buddy?

Onboarding workflows break down most frequently due to ambiguous ownership. Defining distinct, non-overlapping responsibilities across key stakeholders ensures critical tasks are never missed.

Table 3: Onboarding Ownership & Accountability Matrix

How Can SMEs Keep Onboarding Simple with Software?

SMEs do not require overly complex enterprise systems to execute onboarding effectively—they require consistency. Adopting a single, standardized framework combined with modern employee onboarding software eliminates operational confusion and ensures seamless execution.

1. Standardize the workflow: Utilize one consistent 30-60-90 checklist template for every hire across full-time and contract roles.

2. Assign clear ownership: Confirm stakeholder accountability for every task prior to the candidate’s start date.

3. Automate administrative tracking: Leverage employee onboarding software to send automated reminders, collect digital signatures, and track milestone completion.

4. Maintain visibility: Ensure progress checklists remain accessible to both the new hire and their manager in a shared portal.

Standardize Your SME Onboarding Today

Eliminate guesswork and early attrition with structured onboarding workflows. Experience how ABStart HRMS simplifies 30-60-90 day milestone tracking, automates compliance paperwork, and empowers growing teams starting at just ₹99/employee.

Get a Free Custom Demo of ABStart HRMS

Sources & Benchmark Compliance References:

1. TalentCo HR Master Context & Strategy Primer — ABStart HRMS Dataset (Entry pricing ₹99/employee; 30-60-90 retention framework).

2. Onboarding Intelligence & Turnover Dataset — Early turnover metrics (20%-22% in first 45 days, 30%+ in 90 days; replacing costs 90%-200% of annual salary in ₹).

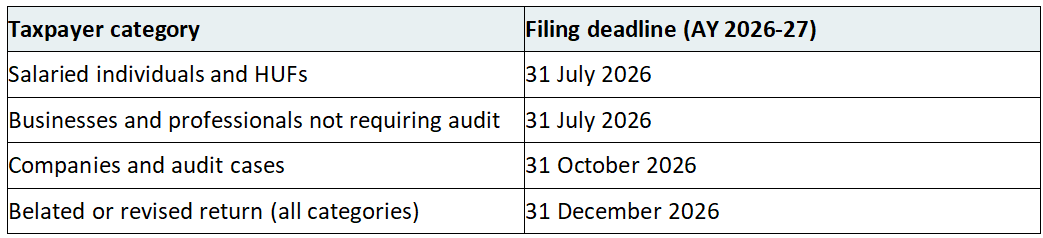

3. Indian Statutory Tax Guidelines — Section 194C/194J vs. Form 16 / Provident Fund compliance rules.

TalentCo HR Services LLP is an HR consulting and solutions company offering services across HR operations, compliance, liasoning, payroll management, and HR technology through its proprietary platform ABStart. This article is intended for general informational and educational purposes only. Labour laws, tax regulations, and compliance requirements are subject to change based on government notifications and jurisdictional updates. Readers are advised to independently verify current regulations or consult qualified professionals before making any business or financial decisions.